![]()

The

Bank of Canada

‘s benchmark

interest rate

has remained at 2.75 per cent since March 12, but the stability hasn’t given young Canadians much relief when it comes to their bills.

Canadians aged 18–34 are taking drastic measures to make ends meet, including high-interest short-term loans when other strategies fail, according to a recent report from the Credit Counselling Society (CCS).

“A steady interest rate doesn’t undo years of financial strain,” CCS chief executive Peta Wales said

in a news release.

“Many young Canadians are already deep in debt. They’re borrowing small amounts just to cover essentials, and over time, those borrowing decisions stack up.”

The number of young Canadians to reach out to CCS has climbed seven per cent since 2023, now amounting to 25 per cent of all clients. The survey also reported that they face an average debt load of $24,000, up nine per cent from 2023.

“The sheer volume of people in their 20s and 30s we’re hearing from speaks to how much financial pressure they are feeling from their mounting debt,” said Isaiah Chan, a vice president at CCS. “They’re doing what they can — working, budgeting, cutting back — but it’s not enough to offset today’s cost of living.”

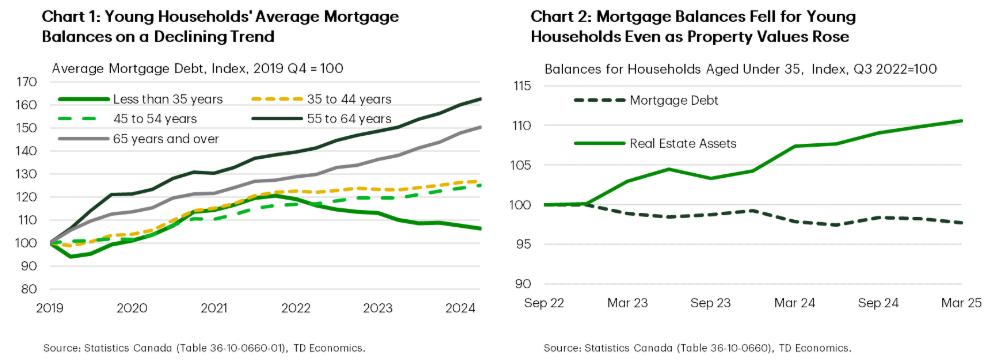

While young Canadians struggle with overall debt,

mortgage debt

appears to be on the decline.

A recent report from TD Economics

shows that mortgage balances among Canadians under age 35 has dropped, while those of all other age groups have risen.

There are several possible explanations, the report said, including younger Canadians opting for less expensive homes when entering the

housing market

or downsizing due to cost pressures.

The report also points to the possibility of young Canadians receiving mortgage help from older relatives. Older Canadians have taken on more debt, but data doesn’t show a spike in new investment properties or renovations, meaning the debt is is attributable to something else.

A 2021 study from Statistics Canada showed that 17.3 per cent of homeowners born in the 1990s co-owned with their parents, while 20 per cent of first-time home buyers were gifted a down payment, according to the Bank of Canada.

Those struggling to pay down their debt may have to wait for some help as

economists said last week

that any movement on rates in September is unlikely, though it’s unclear what might happen with the other two rate announcements in 2025.

CCS is urging anyone feeling overwhelmed with debt to reach out for professional help.

“You don’t need to hit rock bottom to get help,” Chan said. “If you’re unsure what to prioritize, how to juggle payments, or even what solutions are available to you, that’s exactly when to talk to someone. You don’t have to figure it out alone.”

Sign up here to get Posthaste delivered straight to your inbox.

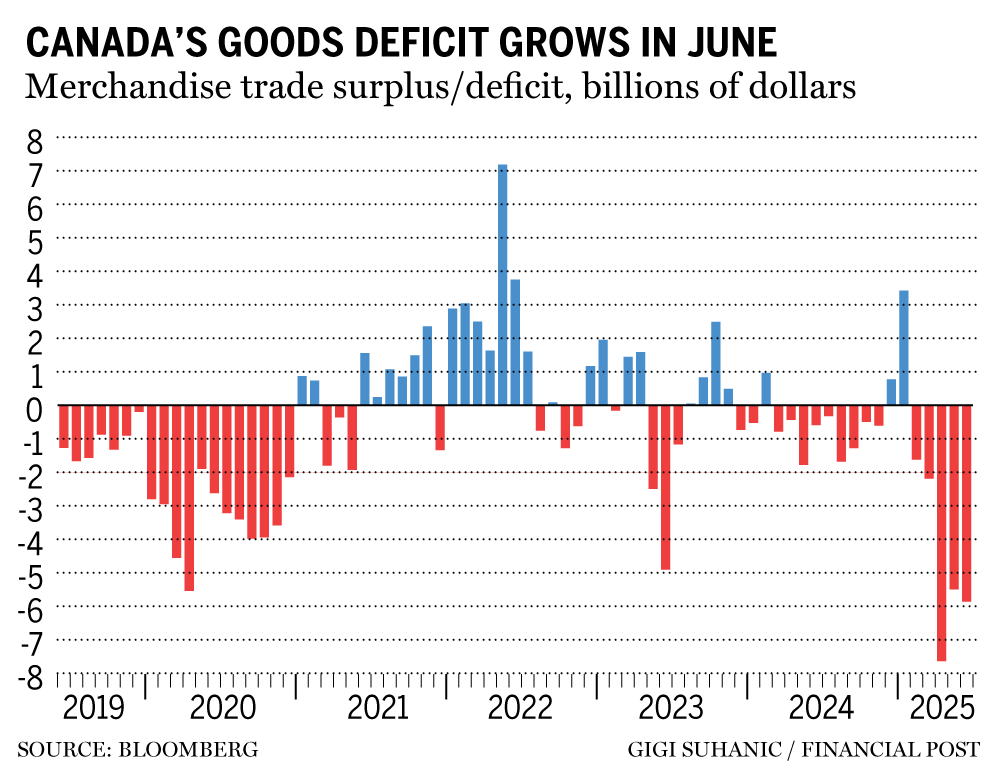

The latest trade numbers shows that

U.S. tariffs

are taking a toll on exporters, particularly in the steel, aluminum and automobile industries.

Statistics Canada data released Tuesday shows Canada’s trade deficit ballooned to $5.9 billion in June,

from $5.5 billion in May.

“Canada’s deficit in goods trade was little changed in June, albeit with plenty of moving pieces in the detail due to U.S. tariff policy,” Andrew Grantham, an economist with CIBC Capital Markets, said in a note.

Exports to the U.S. fell 12.5 per cent year-over-year, while imports from the U.S. were down 4.2 per cent.

Read more here.

- Today’s data: U.S. global supply chain pressure index for July

- Earnings: Novo Nordisk A/S, McDonald’s Corp., Walt Disney Co., Uber Technologies Inc., Shopify Inc., Sony Group Corp., DoorDash Inc., Brookfield Asset Management, Thomson Reuters Corp., Airbnb Inc., Manulife Financial Corp., Honda Motor Co. Ltd., Nutrien Ltd.

- Canada’s trade struggles to ‘find new footing’ as exports to U.S. drop 12.5%

- Here’s why the CRA should keep taxing tips even as the U.S. shies away from it

- Canada Post workers reject ’final offers’ — what happens next?

- Brookfield buys stake in Duke Energy’s Florida utility for $6 billion

Regulators are warning consumers to be careful about taking financial advice from online influencers or so-called “finfluencers.” Financial planner Jason Heath says that while the criticism is mostly justified it also ignores some of the benefits of following financial influencers and some of the problems with relying solely on the financial industry itself.

Find out more

McLister on mortgages

Want to learn more about mortgages? Mortgage strategist Robert McLister’s

Financial Post column

can help navigate the complex sector, from the latest trends to financing opportunities you won’t want to miss. Plus check his

mortgage rate page

for Canada’s lowest national mortgage rates, updated daily.

Financial Post on YouTube

Visit the Financial Post’s

YouTube channel

for interviews with Canada’s leading experts in business, economics, housing, the energy sector and more.

Today’s Posthaste was written by Ben Cousins with additional reporting from Financial Post staff, The Canadian Press and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at

posthaste@postmedia.com

.

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here

Posthaste: Despite stable interest rates, young Canadians struggle to pay the bills

2025-08-06 12:00:23